After 18 months of astronomical price increases for construction materials, market watchers are tracking some supply chain developments that could moderate costs. But widespread relief from high prices, sudden price changes plus slow and erratic delivery times is not imminent nor certain.

“The story lingers, the pandemic lingers, the inflation lingers and the shortages linger. That’s where we are right now,” said Anirban Basu, Chief Economist for Associated Builders and Contractors (ABC).

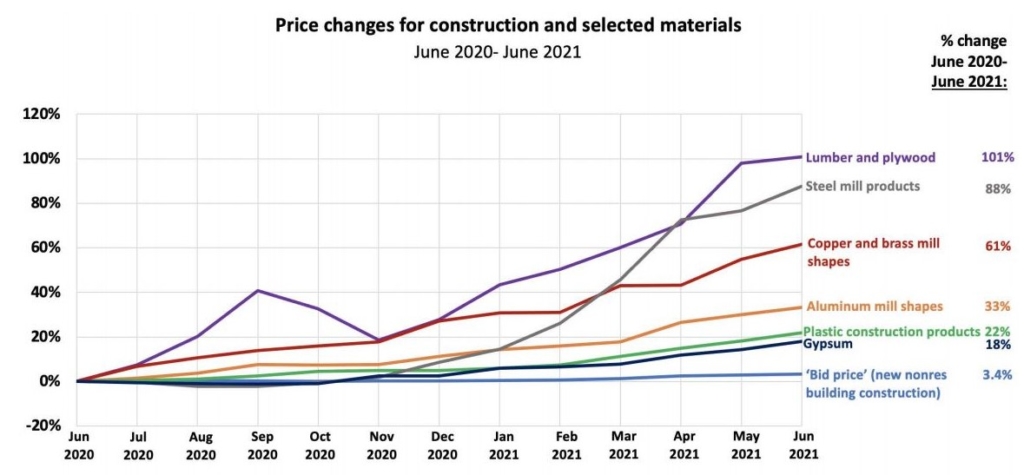

The U.S. Bureau of Labor Statistics’ Producer Price Index showed that total nonresidential construction input prices increased 23.4 percent from July 2020 to July 2021. That included price increases of 108 percent for steel, 101 percent for lumber and plywood, 61 percent for copper and brass products, 33 percent for aluminum, 22 percent for plastic construction products and 18 percent for gypsum.

From June 2020 to June 2021, prices for construction materials experienced what some economists describe as astronomical increases. Some prices are beginning to level off or decline and producer capacity is increasing, Forecasters believe that could lead to lower prices in 2022, but caution that the supply chain is still vulnerable to disruptions by Covid or other factors. That would create high and changeable prices for many months yet.

“The presumption continues to be that at some point global supply chains become better organized, shortages dissipate and prices return to something closer to pre-pandemic levels, including prices for construction input,” Basu said. Considering the strength of the economic recovery, ongoing federal stimulus, pent-up savings and improvements (if uneven) in the pandemic, “it should be the case that that by the fourth quarter of this year, there should be significant improvement in both economic activity and input prices. The supply chains should come back to life… But there’s a lot of room between the joints on projections at this time.”

There are some signs of price and supply chain improvements on the horizon. For example, this summer the price of softwood lumber fell significantly below its mid-pandemic market high.

“The trajectory of softwood lumber prices probably provides us with some insight into what is going to happen with other construction materials going forward,” Basu said. “It is said the cure for high prices are high prices. High prices induce suppliers to step up production in the short term, invest in longer term capacity and increase the quantity shipped.”

Copper prices also eased somewhat this summer as supply increased “and many of the steel manufacturers say they will have more capacity coming onstream in the next few months,” said Ken Simonson, Chief Economist for Associated General Contractors (AGC).

Petrochemical plants in Texas, which incurred extensive damage during the deep freeze and power failure in February, are resuming full operations. That should significantly improve the availability and price of resins, adhesives and plastics that go into a wide variety of construction products, Simonson said.

Meanwhile, a variety of construction materials suppliers are looking to re-shore some of their production capacity to the United States both to counter the volatility of an international supply chain and to avail of favorable tariff arrangements created by the USMCA trade deal, Basu said.

“We are seeing signs that some prices are cresting and heading back down. I think there is increased probability that prices will settle down over the next six to nine months,” said Kermit Baker, Chief Economist for the American Institute of Architects (AIA).

“But there is still going to be a lot of volatility and a lot of challenges for contractors in the next few quarters,” Simonson said. “All industries seem to be struggling to get enough workers to operate at full capacity, including lumber mills, steel mills and other manufacturers and fabricators.”

Transportation networks are still struggling with shortages of shipping containers, ships, docking space, marine crews and truck drivers, he added.

That strained situation combined with the depleted inventories of construction materials means that any localized problem — such as a hurricane, a tornado or Delta surge that cripples some manufacturing facilities — could have inordinate impacts on availability and price of supplies.

Economists warn that the construction industry and their clients will likely have to address another financial strain once materials prices improve and construction activity increases.

“As the market recovers, construction labor is going to become a huge issue,” Baker said.

Construction companies, which have struggled for years to attract sufficient new workforce, now face an added staffing challenge.

Historically, entry-level construction jobs have paid significantly higher (10 percent on average) than entry-level jobs in other industries. However, decisions by warehouse operators, retailers, hospitality companies and others to increase their minimum wage to $15 or above are narrowing that gap and potentially shrinking the pool of new talent for contractors. At some point, Baker said, that shortage could force contractors to raise wages, invest in expanded training programs and adopt new technologies, and those expenses will have to be added to project prices.